The 721 Exchange UPREIT Exit Strategy for Delaware Statutory Trust Investors Explained

One of the most important questions Delaware Statutory Trust real estate investors need to ask themselves is, “What is my long-term, exit strategy?”

Most Delaware Statutory Trust (DST) investments are typically held for approximately 5-10 years (although it could be shorter or longer). After that, the DST investment will typically go “Full-Cycle”, a term used to describe a DST property that is purchased on behalf of investors and then after a period of time is sold on behalf of investors.

For more information on the Delaware Statutory Trust full-cycle event, make sure to listen to this informative podcast. While the two most common exit strategies for DST investors include cashing-out and paying taxes or continuing with another 1031 Exchange, Cove Capital Investments can potentially offer investors a third exit option: a 721 UPREIT.

Once your DST investment goes full-cycle, investors need to evaluate what their next investment move should be, including considering the 721/UPREIT option.

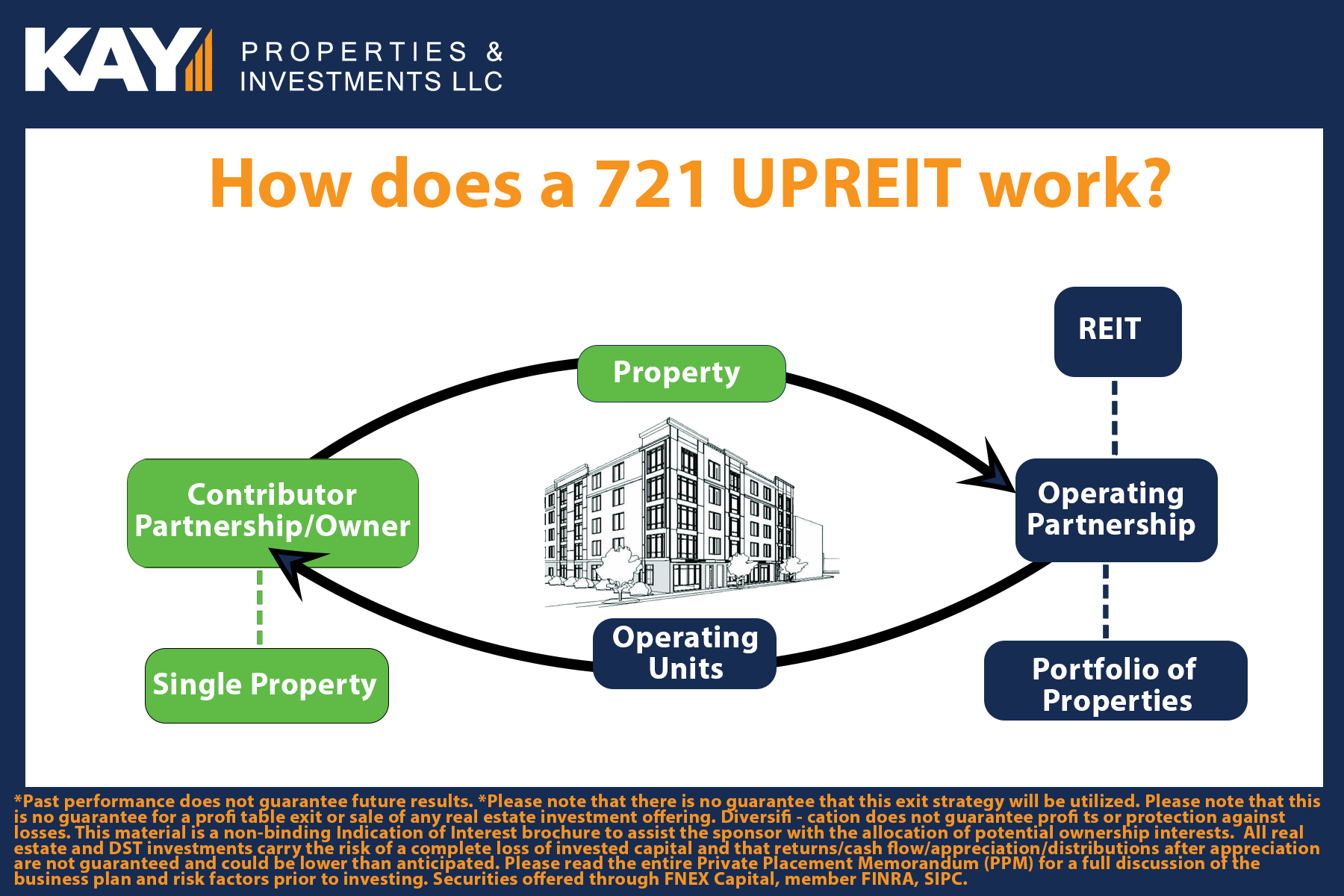

What is a 721 UPREIT Exchange?

The term “UPREIT” is short for Umbrella Partnership Real Estate Investment Trust, which is an operating partnership subsidiary of a REIT that holds and operates real property. Section 721 of the Internal Revenue Code allows owners of real estate property to contribute, on a tax deferred basis, their physical property to a partnership, in exchange for interests in the partnership (a 721 Transaction). This structure allows holders of real estate to exchange real property for economic interest in the REIT in the form of operating partnership units by contributing that property to the partnership in a 721 Transaction. The operating partnership units have economic rights that are identical to the rights of the shares of the REIT, and after a designated holding period can be, if the investor chooses to, converted into shares of the REIT (in a taxable transaction) for liquidity purposes. Investors seeking to defer capital gains taxes while increasing diversification in real estate should consider using a 721 Exchange to realize the following potential benefits.

Tax Advantages - When real estate is typically sold, the investor pays taxes on the capital gains realized as well as depreciation recapture. This leaves the investor with less capital for reinvestment. With the 721 exchange, the investor can avoid this hefty tax through a tax-deferred exchange of appreciated real estate for shares in an operating partnership. These operating partnership units are also known as OP Units. Capital gains can be deferred until the investor sells the OP Units, converts the OP Units to REIT shares, or the contributed property is sold by the acquiring operating partnership.

Diversification - Many investors incur concentration risk by owning one property in a single market. REITs tend to own many assets diversified through different markets. The 721 Transaction into a REIT can provide greater diversification for an individual’s portfolio, which may reduce concentration risk.*

Income Potential - Investors potentially will receive income generated through distributions to the holders of the OP Units.

Liquidity - The ability to convert OP Units of the REIT to shares can provide potential liquidity benefits that are not standard with DST or property ownership. Partial or full liquidity may be achieved, potentially depending on availability determined by the company, by converting the OP Units to shares of the REIT.

Estate Planning - Upon death, shares can be equally split and either held or liquidated by the beneficiaries of the trust. Because these shares are passed through a trust, the beneficiaries receive a step-up basis and can avoid capital gains taxes and depreciation recapture. One Important Caveat for Investors Interested in 721 Exchanges is that REIT shares themselves are not eligible to be used in a 1031 Exchange, and therefore once a 721 Exchange is completed, this is the end of the line for deferral of capital gains taxes. If the shares of the REIT are sold, or the REIT sells a portion of the portfolio and returns the investor’s capital, the investors will be required to recognize any capital gains or loss when they fi le their taxes.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager

1 minute

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

A video-sharing platform for users to upload, view, and share videos across various genres and topics.

This cookie stores your preferences and other information, in particular preferred language, how many search results you wish to be shown on your page, and whether or not you wish to have Google’s SafeSearch filter turned on.

10 years from set/ update

YSC

Registers a unique ID to keep statistics of what videos from YouTube the user has seen.

Session

DEVICE_INFO

Used to detect if the visitor has accepted the marketing category in the cookie banner. This cookie is necessary for GDPR-compliance of the website.

179 days

LOGIN_INFO

This cookie is used to play YouTube videos embedded on the website.

2 years

VISITOR_PRIVACY_METADATA

Youtube visitor privacy metadata cookie

180 days

GPS

Registers a unique ID on mobile devices to enable tracking based on geographical GPS location.

1 day

VISITOR_INFO1_LIVE

Tries to estimate the users' bandwidth on pages with integrated YouTube videos. Also used for marketing

179 days

You can find more information in our Privacy Policy and .